Partnering in Digital Transformation, one client at a time

Services:

Industries:

To think of a digital wallet as just a purchase method is a simplistic reductionism. Technology is revolutionizing the way we send, receive, spend and save money.

Agreeing on and buying a friend’s birthday gift can be a challenging task. Cecilia told us that every time she and her friends decide to buy a birthday gift as a group things get complicated: collecting the money is hard, someone always overpays and ends up covering for the absent-minded and procrastinators.

There are all sorts of discrepancies when choosing the gift and splitting the bill and settling outstanding debts are usually uncomfortable tasks.

Miguel has a similar problem: in each fishing trip he has taken with his former university classmates for the past 25 years, the distribution of expenses has been cumbersome and inefficient. The moment of balancing debts and expenses obscures the harmony of the holidays, and generates doubts and discussions.

The e-commerce company that hired Giro54 to innovate their digital wallet had a blunt request: to rethink the user experience without the restrictions that normally affected its in-house teams and approach the project in an experimental way, integrating functionalities that would be attractive for early adopters while still being easy to use and engaging enough to enhance its chances of going viral.

In the early stages of the project –the deep dive when we research the future users’ contexts, needs and frustrations– we observed that the social side of money is one of the main aspects to consider.

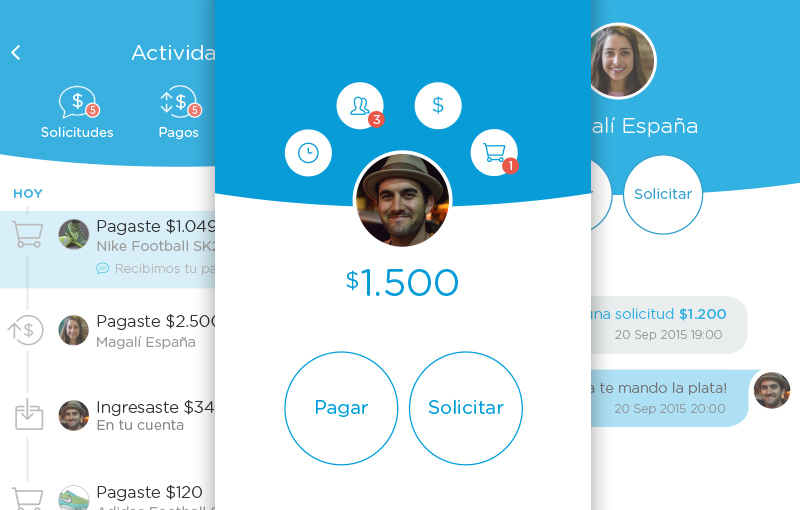

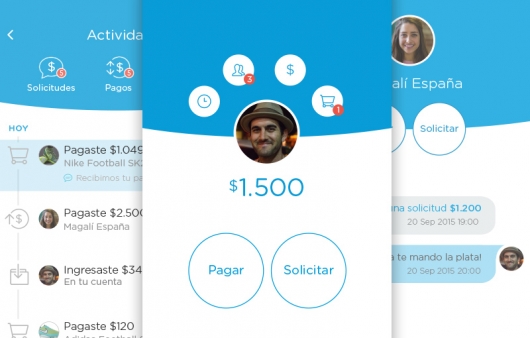

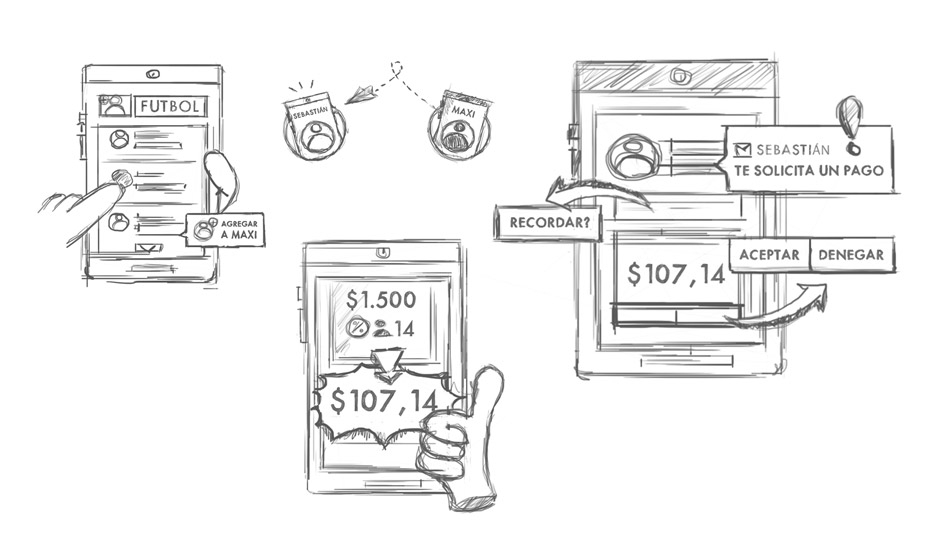

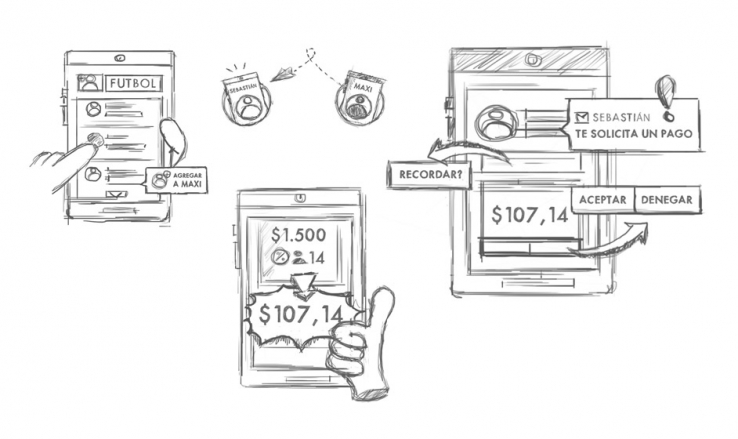

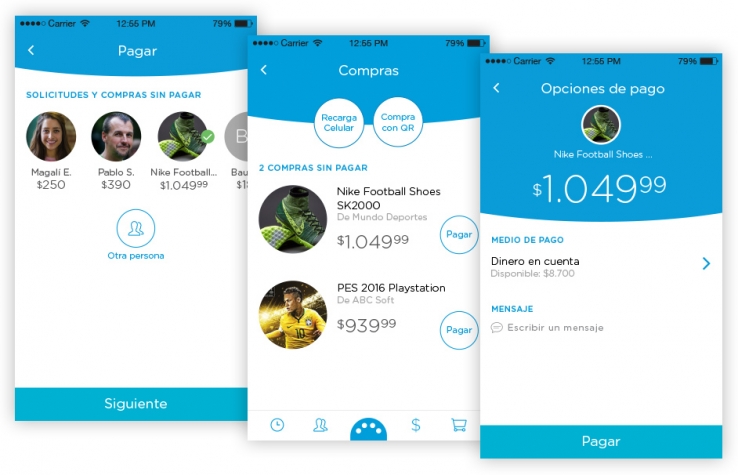

We designed an electronic wallet focused on the social interactions associated with the exchange of money: requesting and sending money to other people, distributing expenses equally in a group, raising funds for a charitable action.

Applying user-centered design techniques, we developed personas –user profiles created from field research and analysis– and outlined their respective “user journeys”. This allowed us to visualize the interactions clearly, detect possible frictions and reduce them to a minimum. For example, security and trust were mentioned as the main concerns among interviewees.

We looked for a solution that would take advantage of the concepts that were already familiar to the users, while also maximizing the technical features of a fintech mobile app: instead of asking for the username and password with each transaction, we use a numeric PIN (the usual verification method for ATMs). In top-of-the-line smartphones, PIN entry is replaced by a simple gesture on the fingerprint sensor that uses biometric data for authentication.

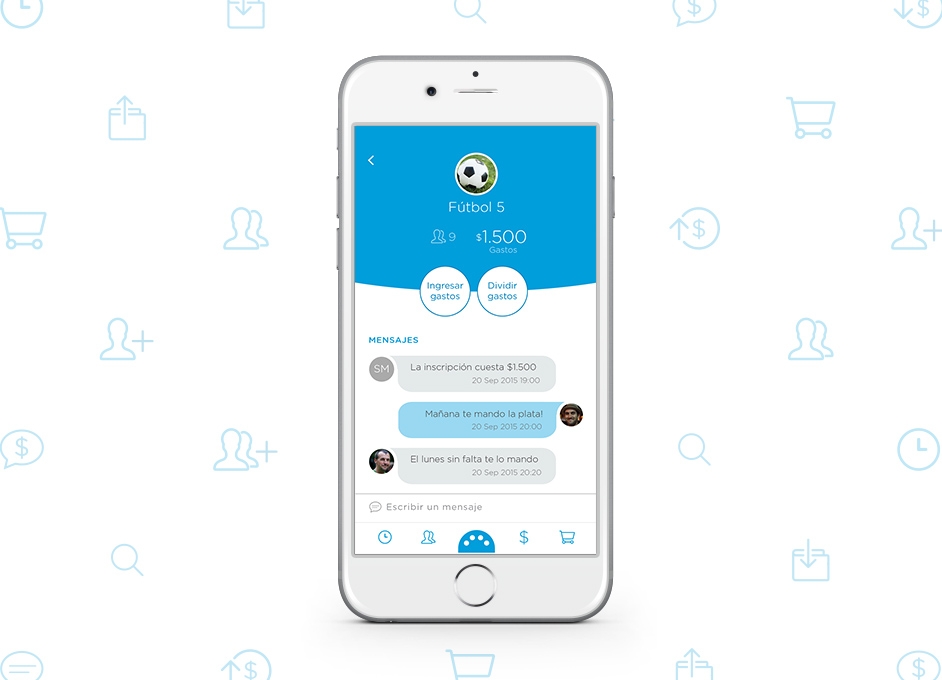

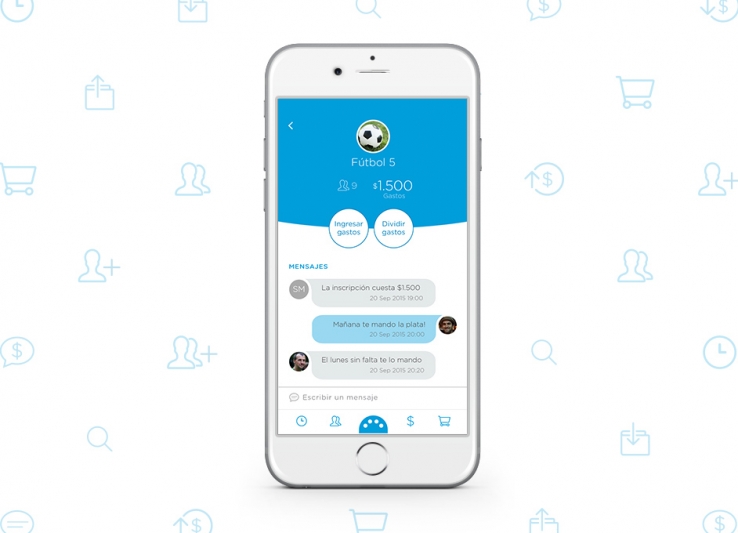

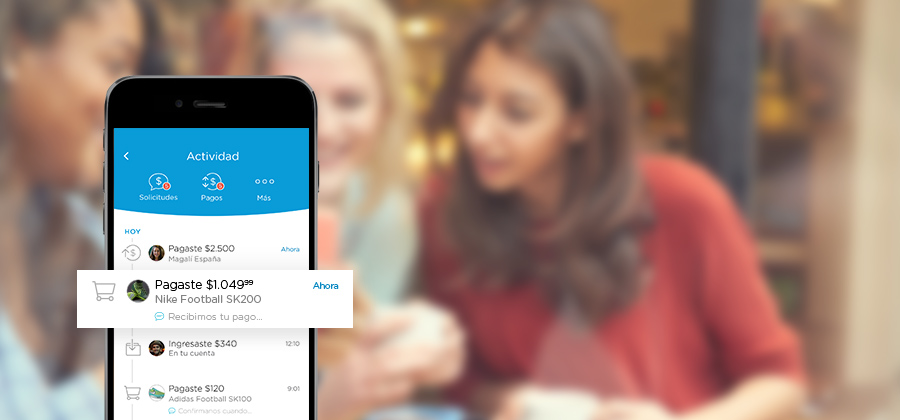

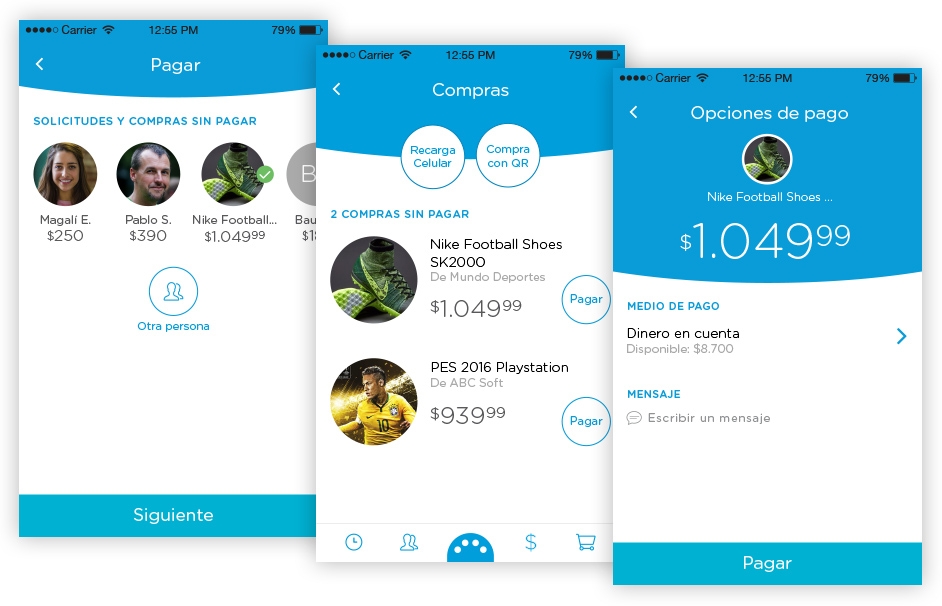

The result is a mobile app with a minimalist design that integrates a variety of features that are visualized in a simplified way with two main functions: Pay and Request money. Each payment can be addressed to one or several recipients, splitting the bill into parts and making the task of paying off group debts much simpler. We integrated social functionalities such as messages, reminders, and groups of people.

This app transformed the experience of splitting charges and collecting money for groups like Cecilia’s and Miguel’s. It automatically calculates who owes how much and to whom based on their contributions, sends payment reminders and allows members to pay off their share of the bill without friction, thus allowing the group to enjoy their vacations and celebrations without monetary distractions.

Would you like to know more about our projects and services?

Contact us Partnering in Digital Transformation, one client at a time

A Fintech start-up with social conscience, to realize the promise of greater community well-being and development

Transforming the casting experience with a disruptive platform.

Licencia Creative Commons - Atribución – No Comercial – Sin Obra Derivada 4.0 Internacional